Authored by Lance Roberts via RealInvestmentAdvice.com,

In their policy announcement last week, the members of the FOMC claimed:

“Information received since the Federal Open Market Committee met in May indicates that the labor market has continued to strengthen and that economic activity has been rising moderately so far this year.”

Economic data has continued to remain extremely soft given the rise in confidence. We addressed previously that while the “soft data” was hitting the highest levels seen since the “Great Recession,” actual economic activity had failed to catch up. As noted on last week:

“For the 13th straight week, US economic data disappointed (already downgraded) expectations, sending Citi’s US Macro Surprise Index to its weakest since August 2011 (crashing at a pace only beaten by the periods surrounding Lehman and the US ratings downgrade). The last time, Us economic data disappointed this much, Ben Bernanke immediately unleashed Operation Twist… but this time Janet Yellen is hiking rates and unwinding the balance sheet?”

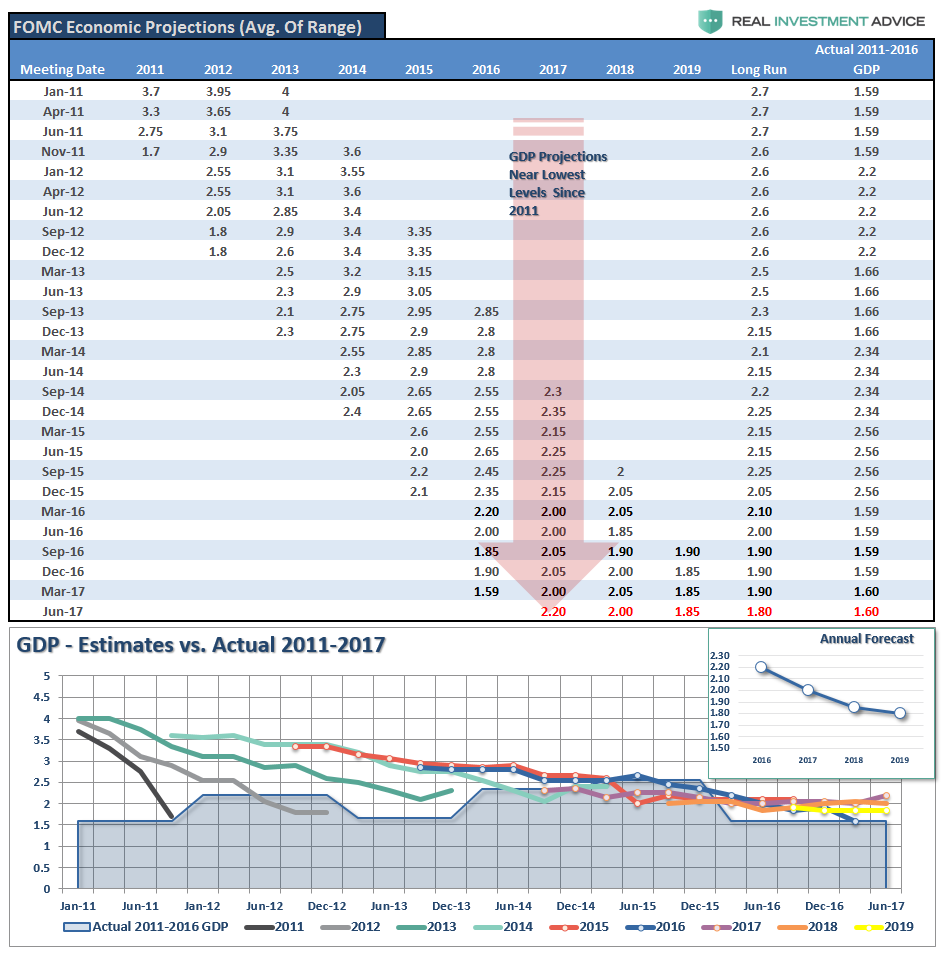

This is quite confusing, considering the Fed is supposed to be “data dependent.” Ever since 2011, I have tracked the Fed’s economic forecasts relative to reality. If they are using economic data to guide their forecasts and policy actions, the following table and graph should scare you.

However, despite the clear evidence that economic growth is hardly running at levels that would be considered “strong” by any measure, the Fed is “tightening” monetary policy. This is ironic considering the ENTIRE PURPOSE of TIGHTENING monetary policy is to SLOW economic growth to keep inflationary pressures at bay.

Neal Kashkari also noted the disconnect between Fed policy and the economy:

“At the same time the unemployment rate was dropping, core inflation was also dropping, and inflation expectations remained flat to slightly down at very low levels. We don’t yet know if that drop in core inflation is transitory. In short, the economy is sending mixed signals: a tight labor market and weakening inflation.”

Kashkari is right in worrying that the Fed is placing too much faith on the Phillips Curve which predicts a tighter reverse relationship between the unemployment rate and inflation than has actually been seen in recent years. This is particularly the case given the problems with the underlying U-3 employment rate calculation as discussed just recently. To wit:

“The Bureau of Labor Statistics (BLS) has been systemically overstating the number of jobs created, especially in the current economic cycle. Furthermore, the BLS has failed to account for the rise in part-time and contractual work arrangements, while all evidence points to a significant and rapid increase in the so-called contingent workforce as full-time jobs are being replaced by part-time positions, resulting in double and triple counting of jobs via the Establishment Survey.

Lastly, a full 93% of the new jobs reported since 2008 and 40% of the jobs in 2016 alone were added through the business birth and death model – a highly controversial model which is not supported by the data. On the contrary, all data on establishment births and deaths point to an ongoing decrease in entrepreneurship.”

Neal goes on to identify the risk:

“In the 1970s, that faith led the Fed to keep rates too low, leading to very high inflation. Today, that same faith may be leading the Committee to repeatedly (and erroneously) forecast increasing inflation, resulting in us raising rates too quickly and continuing to undershoot our inflation target.”

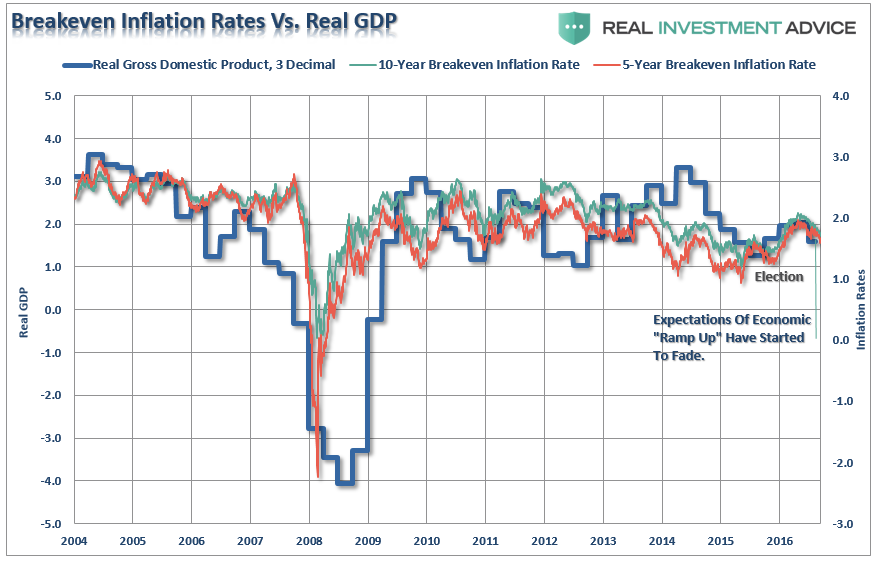

However, one really needs to look no further than the bond market which is also screaming the Fed is once again, as they always have, making a monetary policy mistake. The chart below shows, GDP as compared to both the 5- and 10-year inflation “breakeven” rates.

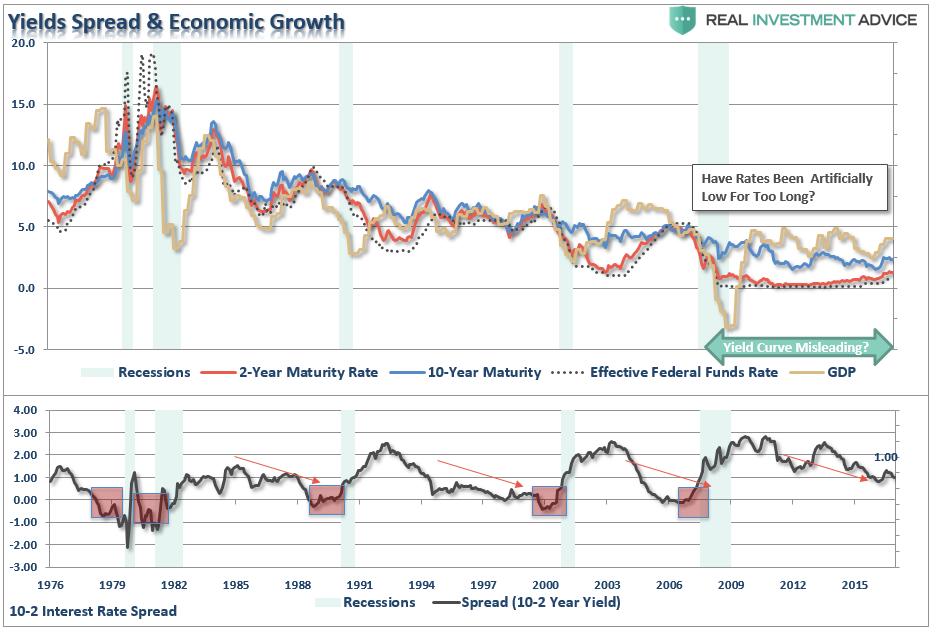

The spread between the 10-year and 2-year Treasury rates, historically a good predictor of economic recessions, is also suggesting the Fed may be missing the bigger picture in their quest to normalize monetary policy. While not inverted as of yet, the trend of the spread is clearly warning the economy is much weaker than the Fed is suggesting.

While none of this suggests a problem is imminent, nor does it RULE OUT higher highs in the markets first, there is mounting evidence the Fed is headed towards making another mistake in their long line of creating “boom/bust” cycles.

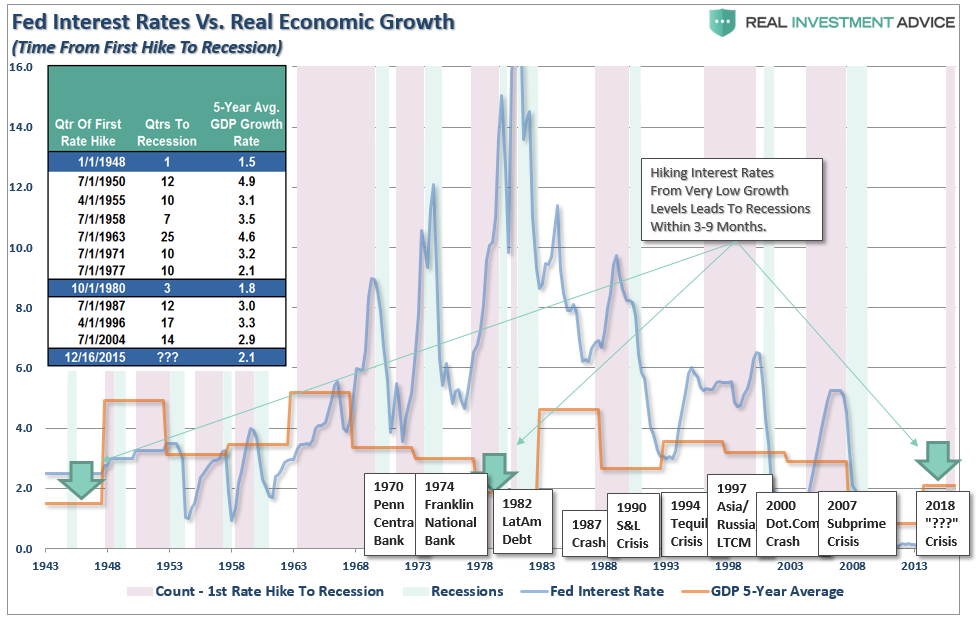

Looking back through history, the evidence is quite compelling that from the time the first rate hike is induced into the system, it has started the countdown to the next recession. However, the timing between the first rate hike and the next recession is dependent on the level of economic growth at that time.

When looking at historical time frames, one must not look at averages of all rate hikes but rather what happened when a rate hiking campaign began from similar economic growth levels. Looking back in history we can only identify TWO previous times when the Fed began tightening monetary policy when economic growth rates were at 2% or less.

(There is a vast difference in timing for the economy to slide into recession from 6%, 4%, and 2% annual growth rates.)

With economic growth currently running at THE LOWEST average growth rate in American history, the time frame between the first rate and next recession will likely not be long.

The Federal Reserve is quickly becoming trapped by its own “data-dependent” analysis. Despite ongoing commentary of improving labor markets and economic growth, their own indicators are suggesting something very different.

While the Federal Reserve may hike interest rates simply to “save face,” there is indeed little real support for them doing so. Tightening monetary policy further will simply accelerate the time frame to the onset of the next recession. In fact, there have been absolutely ZERO times in history that the Federal Reserve has begun an interest-rate hiking campaign that has not eventually led to a negative outcome.

While the Federal Reserve clearly should not raise rates further in the current environment, it is clear they will remain on their current path. This is because, I believe, the Fed understands that economic cycles do not last forever, and we are closer to the next recession than not. While raising rates will accelerate a potential recession and a significant market correction, from the Fed’s perspective it might be the ‘lesser of two evils. Being caught near the “zero bound” at the onset of a recession leaves few options for the Federal Reserve to stabilize an economic decline.

In other words, they already likely realize they are screwed.

source http://capitalisthq.com/data-says-fed-is-making-a-mistake/

No comments:

Post a Comment